Ruifang Fund: Some thoughts about value investment in the new period

Author:China Fund News Time:2022.08.31

Value investment has been continuously improved from outstanding investors such as Graham to Buffett, forming a set of methodology. This system is mainly based on qualitative and quantitative analysis. After the future cash flow of the enterprise is disclosed, the current value of the enterprise is estimated, and investment decisions are made into consideration. For a long time, the traditional value investment brought securities investment from the wrong track of zero -harmony game to the law of price and value interaction. It has important epoch -making significance for the securities market. However, the times are constantly developing, and the capital market is constantly evolving and moving forward. Whether it is a mature market like the United States, or a new market with a special national conditions and the general law of the capital market, some of the thinking methods of traditional value investment. Both have made new challenges.

The first is a great misunderstanding of the concept of so -called "underestimation" and "overestimation" in traditional value investment. In investment practice, investors who think of "overestimation" are likely to be because of the lack of subjective cognition that the degree of prosperity is underestimated; and many people think that it is "underestimated" because they do not realize some of them. Folding. In the process, our team also made a lot of mistakes before we realized this. For example, the study of the photovoltaic inverter industry has not estimated its prosperity. At the same time, for the uncertainty of underestimating stocks, aware that the existence of a certain risk does not mean that it can accurately quantify its risk. Therefore, the "underestimation" and "overestimation" of traditional value investment, in today's secondary equity market, is often a lack of staged cognition.

In the process of gradually iterating the investment and research ideas, our team is increasingly opposed to the saying of "overestimating" and "underestimation". We believe that with the mentality of "overestimating" and "underestimation" It is also easy to become a speculation, which is actually playing with the market. With the evolution of the market, this game will inevitably become more and more difficult. Under the guidance of "overestimation" and "underestimated" investment logic, many people just throw coins in the market differences, even if it proves that it is right or wrong afterwards. In addition, this investment logic also easily leads to a problem: losing awe of the market during investment decisions. Because investment activities are carried out with an overestimated and underestimated mentality, it is bound to be the psychology of trying to defeat the market with a strong attitude. And if it is not for long -term experience and outstanding cognition of related fields, this mentality is often not a kind of wisdom.

Secondly, the concept of safety margin has actually become a pseudo -proposition. The logic of security margins is an effective analysis idea in the early days of traditional value investment, but today in the information age, the marginal margin has become more and more subjective and rigid thinking model. In today's investment practice, if investors are subjectively believed that the security margin is very large and the confidence is full of heavy warehouse buying, it may only be caught in a cognitive blind spot similar to "underestimated" thinking. This kind of cognitive blind zone may not have a deep understanding of related uncertainty and risks. Even if sometimes it is wrong, it is impossible to do it. Undertaking the risks other than their cognition without knowing it. Another common security margin is that the development of enterprises is not isolated. The so -called security margin is very fragile when geopolitics and macro -liquidity changes. Because in major political and economic changes, the prospects of the internal value of the enterprise have actually produced uncertainty. This uncertainty cannot not affect the expectations and pricing of the capital market. Forcibly using so -called fear and greedy tone to try to defeat this difference is not a good solution. Because it is unknown, it is unknown, and it is impossible to have no fear. At this time, investors need to make judgments and decisions on the uncertainty of the macro level or event category. When the investor's investment result is determined by the macro -level politics and economic events, the safety under the initial analysis of the security assumptions under the assumptions of the stability assumption is assumed to be safe. The border is often no longer important or even insignificant.

Another common problem of traditional value investment is the so -called "growing with excellent companies". Without meticulous and quantitative analysis, it is mainly hoped that time to digest the high valuation of the company's phase, it may work in the past, but it will only become more and more difficult in the future. When the flow, integration of information, and the level of market participants are getting higher and higher, the secondary market has evolved faster and faster, and the market price efficiency is getting higher and higher. Generally, buying excellent companies at a lower price or even so -called reasonable price There will be fewer and fewer opportunities. In addition, we should clearly aware that excellent companies are often the products of the era of the times. Many outstanding companies that have proved their own companies have gradually moved towards mediocre or even shattering in new industry changes. The concepts of "excellent", "moat" and "core competitiveness" are not static, and most companies are in fierce market competition and industry changes. For example, a leader in a home appliance is excellent in the past, but many thoughts and actions today are obviously no advanced. Without a measure of cocoon breaking, it is difficult for enterprises to return to their previous competitiveness. Therefore, if you cannot combine the development background, industry changes, and management measures of management in the times, dynamic and prudent research and analysis of the operating strategy and tactics of the target company at all stages. The trap, accompanying the excellent company to grow up, actually implies the risk of accompanying the former outstanding company to go to mediocre. We are in an information age. In normal investment activities, investors can easily study listed companies through a large number of public information. The liquidity of the secondary market is generally much higher than the first -level market and other investment activities. The second -level investment with extensive attention must face fierce competition. From this point of view, investors who have high or even unrealistic expectations for investing in the secondary market are very dangerous. Investors, especially fund managers, should not assume that value investment seems to be some kind of wins, and the complexity and arduousness of the investment in the market should be fully revealed to investors in asset management products.

The traditional value investment of the account -based accounting type with high underscular estimation is gradually losing the true meaning of value investment, increasingly subjective, still, speculation, and more and more vulgar. At the same time, the traditional value investment of the accounting type is often not a real long -term investment, because it is difficult to adhere to long -term holdings that are gradually proved to the wrong investment at the actual level, and there is no significance of persistence.

Today, many institutional investors still can't get out of the simplicity accounting traditional value investment. They tend to invest in so -called "underestimation", "overestimation", and "safe margin". "Excellent Company", these investment logic is difficult to adapt to the changes in today's capital market. However, we can also see many excellent active management investors have completed the transformation. Based on the changes of the times and iterate their own investment and research concepts, they use technological changes, industrial transformation, and industry cycle as the starting point of investment to strengthen the macro political and economy Study the proportion of investment decisions. Under in -depth research and thinking, dare to dare to brightly lighten the market, constantly learn lessons, actively embrace the uncertainty in social and economic changes, and achieve long -term holding with correct and forward -looking fundamental analysis as the cornerstone. We believe that such investment concepts are more in line with the needs of the development of the times, and ultimately meet the needs of the development needs of the times, and the harvest is also the most richer.

Life is essentially an investment. It has a long -time length of time, and then invests in various activities such as physics, mathematics, politics, economy, art, sleeping, eating, and moving bricks. Life is similar to stock prices. It is difficult to calculate the account beforehand. Only by combining personal efforts with the historical process can we resist the fluctuations and uncertainty of the personal situation. Essence The same goes for the secondary market. (CIS)

""

China Fund News: Everything that reports the fund's attention

ChinaFundnews

Long press to identify the QR code and follow the China Fund News

- END -

Control and innovation information in the semi -annual net profit of 354,600 yuan in the semi -annual profit decreased by 79.65% year -on -year

On August 25, the control information (code: 836166.NQ) released the performance report of the 2022 semi -annual report.From January 1, 2022-June 30, 2022, the company realized operating income of 59.

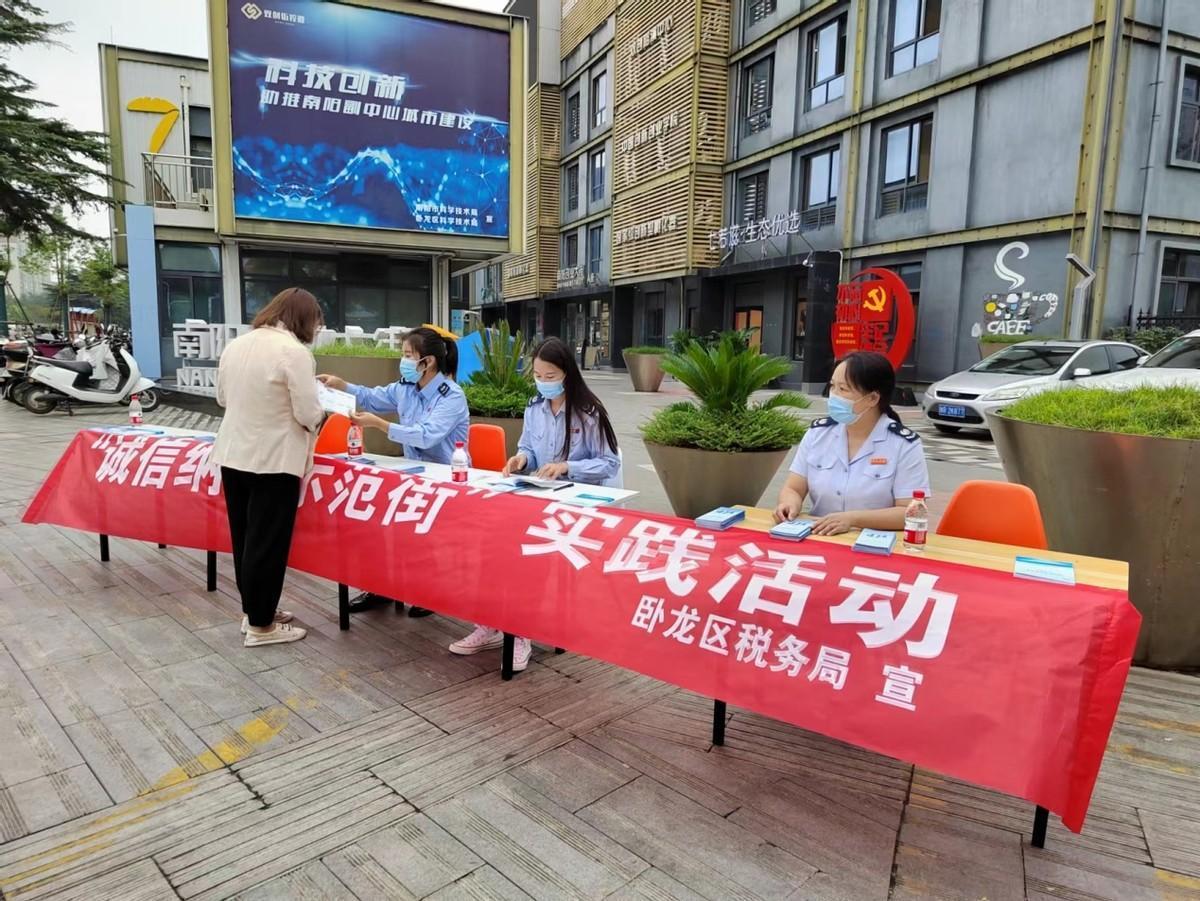

Nanyang Wolong Taxation: Carry out "Integrity Tax Demonstration One Street" practical activity

On the morning of August 31st, the Taxation Bureau of Wolong District, Nanyang Cit...