Audit Observation | Department Budget Examination and Financial Report Audit Coordination Analysis of Audit and Government Department

Author:Audit observation Time:2022.09.07

Government financial report audits are a new type of business facing audit organs. Government financial reports based on the occurrence of power and responsibility have been tried and compiled by trial compilation and preparation. As an important audit work, the budget execution audit has continuously expanded in terms of breadth and depth in recent years. The two can learn from each other in terms of audit content, audit methods, and audit results. The two should be fully considered the organic connection of the audit plan, audit time, audit content, organizational arrangements and strength equipment, integrate audit resources, and improve audit efficiency.

Overview of audit audits of the departmental budget execution and government departments

The final account reports and government financial reports are important contents and carriers for budget execution audits and government financial report audits, respectively. Clarifying related concepts and policy backgrounds help better grasp the nature and similarities of the two audit types.

(1) Conceptual concept

The final account report and government financial report. The department's final account report refers to the comprehensive annual report of all departments in accordance with the relevant national laws and regulations and its performance of the function of fulfilling their functions, reflecting all budget revenue and expenditure results and performance of the departments. Reference and basis for the budget; the goal of government financial reporting is to provide financial reporting users with information such as government financial conditions, operations and cash flow, which reflects the performance of the government accounting subject's public trust. Decisions or supervision and management, including comprehensive government financial reports and financial reports of government departments (see Table 1).

Table 1 The difference between the final account report and the financial report of the government department

The departmental budget audit and government department's financial report audit. The budget execution audit refers to the annual financial budget of the audit authorities at all levels in accordance with the review and approval of the people's congress at the level, and the financial and various budget executive departments and units at the budget should be raised, allocated and used in the budget execution process. The completion of the revenue and expenditure tasks and the audit supervision of the true, legal and benefits of other fiscal and financial revenue and expenditure; the government financial report audit is the audit authority in accordance with legal duties, permissions, and procedures. Government financial report preparation measures and other audit evaluations of government financial conditions and operations.

(2) Policy background

In 2014, the "Notice of the State Council's Reform Plan for the Reform of the Government's Comprehensive Financial Reporting System of the Ministry of Finance and Responsibility of the Ministry of Finance" put forward the requirements of "establishing and improving the government's financial report audit system". In 2019, my country officially implemented the government accounting standard system. In 2020, it officially prepated to formulate government financial reports, and the scope of the establishment covered 108 central departments and 36 places. Twelve of them also tried comprehensive government financial reports. In September 2020, the Audit Office studied and formulated the "Government Financial Report Audit Measures (Trial)", which stipulated the relevant work of the audit authorities. In practice, the Audit Office has conducted a trial on the financial reports of Shanxi Province and some central departments in recent years.

The budget execution audit is the basic responsibility given to the audit authority by the audit law. "Supervision", the budget execution audit has become the annual regular audit task of the audit organs. Since the 18th National Congress of the Communist Party of China, the audit organs have deepened budget execution and final account audits, continuously explored and improved audit organization methods, increased the integration of audit resources, promoted data penetration, and enhanced audit results.

(3) The similarities and differences between the two

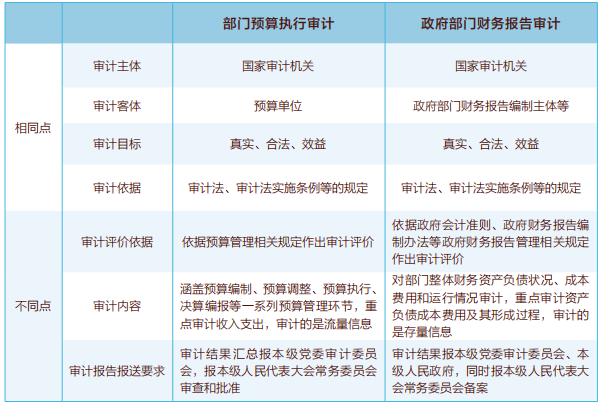

The department's budget execution audit and government departments' financial report audits. The audit subjects are national audit organs, the audit object is the government departments, the audit goals and audit basis are the same, and they can coordinate each other in terms of audit results. However, the two are different in the audit evaluation basis, audit content, and audit reporting mechanism. The departments budget execution audit content covers a series of budget management links such as budget preparation, budget adjustment, budget execution, and final account reports. Focus on auditing revenue expenditures, and the audit is traffic information; the financial report audit of the government department is the status of the overall financial assets and liabilities of the department. Cost costs and operating audit, focus on the cost of asset liabilities and its formation process, the audit is the stock information. The two complement each other to form the whole. The departments budget execution audit results summarize the audit committee of the party committee at the level, and report to the Standing Committee of the People's Congress at this level for review and approval; The committee is filing (see Table 2).

Table 2 The similarities and differences between the audit of the department's budget and the financial report audit of the government department

The necessity, feasibility and main issues of the audit of audit and government departments' financial report audits

According to the "Government Financial Report Audit Measures (Trial)", government financial report audits are included in the management of the annual audit project plan, which can be implemented alone, or in accordance with the budget execution audit and draft final account audits.

(1) The necessity of overall planning

From the perspective of practice, it is necessary to implement the department's budget audit and the financial report audit of the government department. The overall implementation of the two can not only arrange human resources, alleviate the contradictions of insufficient audit power, and avoid repeated audits of the audited unit. At the same time, from the organization and implementation of the two to coordinate with each other and complement the audit content, it also helps improve the audit efficiency and quality. It can formulate relevant work plans and implementation plans, coordinate tasks and key time nodes, coordinate research and planning related issues. The overall adjustment of the audit force, the audit content can be added to each other to improve the audit and efficiency. (2) The feasibility of the two coordinates

The first is to be led by the financial audit leadership group of the audit organs, and has overall conditions in planning and deployment. The departmental budget execution audit and government department's financial report audits are all led by the financial audit leadership group. When studying the next year's audit plan, the two can be planned to plan, make a reasonable arrangement of auditors, formulate an audit implementation plan, or one can also be one. And issued an audit notice.

The second is that the audit object has a high weight, providing a realistic foundation for the two coordinated implementation. The departmental budget execution audit and government department's financial report audit objects are all unit account report statements and project establishment documents. They all pay attention to related content such as accounting processing, state -owned asset management, and financial risks. For example, in terms of inspection of state -owned assets management, a state -owned assets are allocated or non -budget allocation, and the purchase of state -owned assets has not been submitted in accordance with procedures. The illegal construction building hall or office house is a problem that the budget execution audit needs; whether the bottom number of fixed assets is clear Whether the subject is clear, whether the initial measurement and depreciation of the subject are required by the financial report audit of government departments; illegal issues such as lease and illegal disposal are issues that are reflected in both types of audits.

The third is that the audit methods are mainly based on reviewing the accounts, data analysis, interview inquiry, and extension of investigation, which have consistent requirements for the professional quality of the auditors. The method of the department's budget execution audit and the financial report audit of the government department is basically common. All are through interviews to understand the overall situation or a specific situation of some aspects. Related enterprises and other problems are required to have basic professional capabilities in finance, accounting, computer and other aspects. For example, when auditing the assets, the commonly used methods include to inquire about the assets of the unit through interviews, check the asset registration file, asset management information system, asset statistics report, long -term equity investment inspection report, etc. Compare the data of the state -owned asset management information system of administrative institutions, as well as external data such as finance, state -owned assets, and market supervision, and find inconsistent situations.

(3) The main problems faced by the two

First, due to the completion time of the financial reporting of government departments behind the implementation of the implementation of the audit of the budget, the two are difficult in the audit time. The departmental budget execution audit is generally carried out at the end of each year. The single -accounting annual year is the cycle. It is necessary to strictly grasp the audit progress and on -site audit time. The on -site audit time is about December from December to March of each year. The financial report of government departments is generally not completed during this period of time. It is not until the end of May of the following year that the financial report of the government department was submitted to the financial department. If the financial report audit of the government department and the department's budget execution audit arrangement, the government department's financial report audit does not have a carrier and starting point, and it is difficult for the two to achieve coordination in the audit time. In addition, a problem faced is that the audit time of the final account (draft) is limited to the completion time of the draft of the final account to the time of the review and approval time of the Standing Committee of the People's Congress (or the end of the audit of the budget). Not sufficient, there is a certain audit risk.

The second is that the audit goals of the two have different audit goals, which determines that the audit focus on content and the main issues of the audit discovery have their own emphasis, which brings certain obstacles to the connection between the two. Although the content of state -owned asset management and accounting treatment has a certain weight, most of the audit content is determined according to their respective audit goals, and each has its own emphasis. The audit goal of the department's budget execution of audit is relatively macro and more national audit. The audit content pays more attention to the implementation of major policies, the legal compliance of fiscal funds and performance, financial and financial revenue and expenditure, financial risk prevention, and the implementation of the integrity government Discipline, etc. The audit goal of the financial report audit of government departments is more specific, and the content of the financial report audit should focus on whether the scope of the statement is reasonable and the implementation of the government accounting system (specifically including assets, liabilities, net assets, income, expenses and other accounting accounting Documents), whether the reconciliation offsets whether it should be offset, the confirmation standard of capitalization costs, whether the accounting system is connected, and the problems of internal control construction, informatization construction, efficiency, and connection with asset management.

Third, the audit development stage is different, the requirements of the submission objects are different, and the content and form of audit results are different. The department's budget execution audit has been carried out for many years, mature technology and rich experience. It is one of the core contents of the audit work. The audit results are mainly based on the audit report. Report to the People's Congress. The financial report audit of government departments is an emerging type of audit. It is in the stage of exploration and implementation. It has new requirements for auditing technology and professional capabilities. The form of audit reports is still being explored and there is no conclusion. It should be noted that according to the development practice of the financial report audit of the government department, the two are currently coordinated with financial management and financial information audit, and they cannot achieve evaluation opinions on financial reports. Fourth, the functions of the financial report and reporting system need to be improved, and the preparation and reporting system has not yet been shared, which affects the connection between the two data. At present, the editing function and query function of the financial report and reporting system need to be strengthened and improved. The system cannot be edited online. After generating the report, you need to download it to the local editor before uploading. Dimensions and multi -indicator -associated queries affect data comparison review. In addition, there is a system connection to debugging, affecting the accuracy of data. From the perspective of management, the Ministry of Finance's Financial Report Management System and Dating Computing and Report Management System have not yet been shared by Unicom, which is not conducive to the comparison analysis of the data on the audit authorities.

In addition, there are still problems such as weak financial reports, the level of accounting personnel, accounting management, and the complete reliability of accounting information needed to be improved and strengthened.

Realize the path and suggestion of the audit of the department's budget and the financial report of the government department

On the basis of summing up practical experience, this article studies and proposes the implementation of the path and related suggestions of the implementation of the department's budget execution audit and the financial report audit of the government department for reference in practice.

(1) The path of co -ordination of the two

Path 1: Mixed implementation. Under this model, the government department's financial report audits are arranged at the same time in the audit of the department's budget. The financial report audit of the government department not only independent items, but also issued an audit notice, which will be implemented by the same group of auditors to form an audit report. The department's budget execution audit and the financial report audit of the government department at the same time. The same audit team leader and the same chief trial can be implemented in the group. The audit time shall prevail the audit time of the department's budget. During the audit process, not only depending on the problem of budget execution, but also financial treatment issues. According to the working hours, there are different focus at different stages. If the budget execution issues are found in the early stage, the financial reports are found in the later period. The audit found that the team leader and the trial were responsible for classifying, and now they are in a audit report. After the audit site is over, the financial report will be submitted to the financial department, and then checks the information and the form of individual interviews to check the leakage. This model can shorten the audit site time, save audit time and personnel costs, and improve the efficiency of audit; The inspection work is not in place and it is easy to cause the problem to miss the problem.

Path 2: Single independent item implementation. In this model, the single independent implementation department budget audit audit and government department financial report audit. After the department's budget execution audit is over, the financial report audit of the government department is connected. Auditors generally implement the budget execution auditors to fully understand the situation of the audited unit. The audit time generally continues until mid -June, and the government financial report has been compiled. This audit model is further reviewed and sorted out financial report -related issues on the premise of a certain understanding of the budget execution and final accounts of the audited unit to form a audit report. This model audit site has been long time, which has increased the impact on the audited unit to a certain extent. However, some financial reports are used as the starting point. The audit is coherent and complete, and the problem is relatively comprehensive. In this case, the financial report audit of government departments has certain correlation with the department's budget execution audit, but it is also relatively independent.

(2) Suggestions to achieve overall planning

The first is to further improve the relevant laws and regulations of the government's financial report audit, improve the legal level, and clarify the audit content. Internationally, relevant foreign countries generally clarify the government's financial report audits and make detailed provisions in relevant laws. For example, a number of relevant laws such as the US "Government Management Reform Act", "Tax Accountability Act", and the United States Audit Agency Law have clearly stipulated the financial reports and comprehensive financial report audits of government departments. Britain issued the "Government Resources and Accounting Acts" at the parliamentary level to make detailed provisions on the audit of government financial reports, auditing obtaining information, and submission of audit reports. At present, my country's newly revised audit law has not yet made specific provisions on the content of the financial report audit. It is recommended that special regulations documents have regulated the audit of departmental financial reports, comprehensive financial report audits, and clearly clearly make clear audit organization methods, audit reports, audit disclosure, etc. Specific regulations provide a complete basis for government financial report audits.

The second is to further strengthen the application of big data technology in budget execution audit and government financial report audits, optimize the system environment, and strengthen data sharing. First, the financial department should further improve the government financial report management system and optimize the system application environment. All departments and units should combine the needs of the financial reporting of government departments, optimize the system application environment, improve the system software, standardize the scope of reconciliation of financial reports, increase the reconciliation function of the subjects of exchanges and payments, improve the report of reports and reports Accuracy and comprehensiveness. Second, further promote the connection between the accounting accounting system and the financial accounting system of the department. Accelerate the automatic extraction function of the accounting system account book data, automatically generate financial report reports, based on the automatic identification and processing of reporting data, and can automatically identify the creditor's rights and debts and income fees based on the report data. Whether the data is accurate, then manually check to ensure that the data is correct and improve work efficiency. Third, strengthen the interconnection sharing of relevant data such as the financial report of government departments and administrative state -owned assets, and departments' final account reports. It is suggested that the financial department will compile and report the various unicom to realize the horizontal and vertical multi -dimensional and multi -indicator -associated queries to facilitate data comparison, and pay attention to the connection between systems to ensure the accuracy of data. Third, it is recommended that the relevant departments further improve the refinement of refinement of the financial report and reporting guidelines, and advance the financial report report time. It is recommended that the financial department issued a detailed offset operation guide as soon as possible, and promotes the units to fully understand the principles and rules of government financial report offset, and further improve the quality of government financial reports. The specific content, financial analysis specific requirements, and the main points of government financial report review also need to further refine the guide. At the same time, in the case of conditions and maturity of the time, it is recommended that the financial department should try to compile the financial reporting time in advance as much as possible to synchronize it with the audit time of the budget, and to implement the creation conditions for the departments' budget execution audit and government department's financial report audits.

The fourth is to strengthen training and conduct exchanges. Strengthen the experience exchanges between the central department's government financial report audit and the financial report audit of local audit organs, and jointly discuss the methods and methods of promoting the implementation of budget execution audit and government financial report audits. Summarize the local audit agencies that are coordinated by the two, and form a typical case to promote the experience and practices of audit plans, work plans, organizational implementation, audit methods, human arrangements, audit reports, and audit rectification. (Author Yang Yuting Unit Department Audit Research Institute)

Source: "Audit Observation", No. 7, 2022

- END -

In 2022, the 20th cities of the nationwide cities of Lepi Taka will be launched soon

In order to actively respond to the Notice on Further Strengthening the Comprehens...

Lintong: The reform of state -owned enterprises injects new kinetic energy for the development of the construction industry

Since 2020, the reform and development of state -owned enterprises in Lintong Coun...