The two departments issued a clear article to clearly delay the payment of some taxes and fees (with interpretation)

Author:State Administration of Taxati Time:2022.09.14

Ministry of Finance of the State Administration of Taxation

Announcement on the continued delay in paying part of the taxes and fees related to the manufacturing industry

Announcement of the Ministry of Finance of the State Administration of Taxation 2022 No. 17

In order to thoroughly implement the decision -making and deployment of the Party Central Committee and the State Council, and further support the development of small and medium -sized enterprises in manufacturing, the manufacturing small and medium -sized enterprises (including individual wholly -owned enterprises, partnerships, individual industrial and commercial households, the same below) will continue to delay the payment of some taxes and fees policies The announcement of the relevant matters is as follows:

1. Since September 1, 2022, the announcement of the "Announcement of the Ministry of Finance of the State Administration of Taxation on continuing the implementation of the implementation of small and medium -sized enterprises in the manufacturing industry to delay the payment of some taxes and fees (2022 No. 2) has enjoyed the delay of the tax and fees of 50 %Of manufacturing medium -sized enterprises and small and micro enterprises that delay 100%of taxes and fees have continued to extend 4 months after the expiration of the slow payment period for the expiration of the slow payment and fees.

2. Delayed taxes and fees include the period of affiliated in November, December 2021, February, March, April, May, June (monthly monthly) or 2021 In the first quarter and the second quarter (quarterly paid), corporate income tax, personal income tax, domestic value -added tax, domestic consumption tax and attached urban maintenance construction tax, educational expenses, and local education additions, excluding buckles Payment, collection and payment, and taxes paid when applying for invoicing from tax authorities.

3. The delayed taxes paid paid in November 2021 and February 2022 will be paid in the warehouse before the announcement of this announcement after September 1, 2022, and you can voluntarily choose to apply for tax refund (fee) and enjoy the continuous and slow payment policy.

4. After the expiry of the post -end payment period stipulated in this announcement, the taxpayer shall pay the corresponding month or quarterly taxes and fees in accordance with the law. Apply for extension of tax payment.

V. Taxpayers who do not meet the requirements of this announcement and deceive the policies for the enjoying tax payment, the tax authorities will be dealt with seriously in accordance with the relevant provisions such as the "Taxation and Management Law of the People's Republic of China" and the implementation rules.

6. This announcement will be implemented from the date of issuance.

Special announcement.

Ministry of Finance of the State Administration of Taxation

September 14, 2022

Interpretation

Interpretation of the "Announcement of the Ministry of Finance of the State Administration of Taxation on Small and Micro -Enterprises Small and Micro -Enterprises Continue to Delay Paying Part of Taxes and Fees"

In order to support the development of small and medium -sized enterprises in manufacturing, the State Administration of Taxation in the early stage introduced the Ministry of Finance with the Ministry of Finance the manufacturing industry's small and medium -sized enterprises to slowly pay taxes and fees. In accordance with the original settlement policy, from August this year to January next year, the tax -fee payment period has expired one after another. In order to thoroughly implement the decision -making and deployment of the Party Central Committee and the State Council, and continue to help the enterprises to relieve the difficulties, the State Administration of Taxation and the Ministry of Finance and the Ministry of Finance issued the "Announcement of the Ministry of Finance of the State Administration of Taxation on Small and Medium and Micro -Enterprises in the Manufacturing Industry to continue to delay the payment of some taxes and fees (2022" The 17th, hereinafter referred to as the "Announcement"), clearly stated that starting from September 1, 2022, the announcement of the "Ministry of Finance of the State Administration of Taxation on continuing the implementation of manufacturing small and medium -sized enterprises to delay the payment of part of the tax and fees related issues" (2022 "(2022" No. 2) It has enjoyed a manufacturing medium -sized enterprise with a delay of 50%of the tax payment and the manufacturing small and micro enterprises that delay 100%of taxes and fees. The slow payment period has continued to extend 4 months after the expiry of the expiration of the slow payment and fees.

I. What are the specific taxes and fees that stipulates that the "Announcement" specifies?

The tax and fees paid by this "Announcement" include the period of November, December 2021, March, March, April, May, June (monthly monthly) or 2022 In the first and second quarters of the year (paid by quarterly), corporate income tax, personal income tax, domestic value -added tax, domestic consumption tax, and attached urban maintenance construction tax, educational consumption, and local education additional Deduction, payment, and taxation to the tax authority when applying for an invoicing on behalf of the tax authority.

As the tax payment period of the affiliated period in October 2021 and January 2022 has expired, the taxpayer shall be paid in the warehouse in August 2022, and this "Announcement" is not applicable.

The taxes and fees that occur in August 2022 (or the third quarterly paid by the quarter) and the period of the period will be paid normally in accordance with regulations.

2. When will the continued delayed tax and fees stipulated by the "Announcement" should be paid in the warehouse?

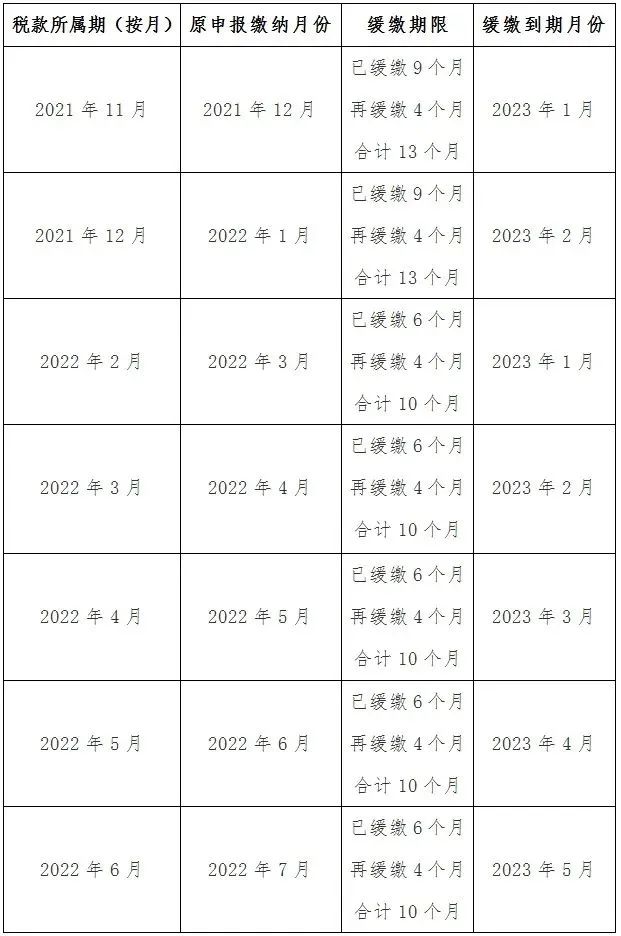

The period of affiliated is November and December 2021 (including the fourth quarter of 2021 taxes paid by the quarter), which continues to extend the taxes and fees on the basis of 9 months (a total of 13 months), respectively, respectively In the warehouse in January and February 2023.

The term of the affiliated period is in February and March 2022 (including the first quarter of 2022 taxes paid by the quarter), and the slow payment and fees of April, May, and June (including the second quarter of 2022) are prolonging On the basis of 6 months, it continued to extend 4 months (total extension of 10 months), and entered the warehouse from January 2023 to May 2023, respectively. See the table below for the specific slow payment period:

(1) Taxpayers who declare taxes on a quarterly basis

(2) Taxpayers who declare taxes on a monthly basis

3. How does manufacturing small and medium -sized enterprises enjoy continuing to delay the payment policy?

In order to facilitate the taxpayer to enjoy the policy, the tax authority has optimized and upgraded the information system. If the manufacturing small and medium -sized enterprises have enjoyed the delay of the tax payment policy in accordance with the announcement of the 2022 announcement, the taxpayer operation is not required after delaying the expiration of the payment period. The payment period is automatically extended for 4 months. Example 1: The taxpayer A belongs to the manufacturing small and medium -sized enterprises stipulated in the announcement of the 2022 announcement, and the relevant taxes and fees are declared on a monthly basis. The period is 9 months, and the original policy will be paid before the application period in September 2022. After the release of this "Announcement", the relevant tax and fees payment period in November 2021 was automatically extended for 4 months. It can be applied for payment and payment of relevant taxes and fees in December 2022 during the January 2023.

If the taxpayer A declares and pays related taxes on a quarterly, the relevant taxes and fees in the fourth quarter of 2021 have been paid in accordance with the regulations, and the period of slow payment is 9 months. According to the original policy, it will be paid before the end of the application period in October 2022. After the announcement of this "Announcement", the relevant tax payment period in the fourth quarter of 2021 was automatically extended for 4 months, which could be paid during the reporting period in February 2023.

Example 2: Taxpayer B is an individual industrial and commercial households that meet the tax slowing conditions. It implements a simple declaration and pays for quarterly. For the relevant taxes and fees that have been slowly paid in the fourth quarter of 2021, the taxpayer does not need to operate to confirm the relevant tax of the relevant tax. In the expense, the tax authorities will not deduct their personal income tax, VAT tax, consumption tax and cities that have been slowed in the fourth quarter of 2021 in the fourth quarter of 2021 in the fourth quarter of 2021. Related taxes and fees continue to be extended for 4 months, and the tax authorities are deducted into the warehouse in February 2023.

4. In November and February 2021, the delayed taxes paid in February 2022 were paid to the warehouse before the release of this announcement after the announcement of this announcement?

Small and medium -sized enterprises in the manufacturing industry in November 2021 and February 2022 delayed the tax paid. If it has been paid in the warehouse before the announcement of the announcement on September 1, 2022, you can voluntarily choose to apply for a tax refund (fee) and enjoy the continuation slowing down. Payment policy.

Example 3: Taxpayer C delays taxes and fees that have paid the affiliated period in February 2022 in accordance with the provisions of the 2022 Announcement of 2022, and have been paid in the warehouse on September 5, 2022. For this part of taxes, you can voluntarily choose to apply for tax refund (fee) and enjoy the continuation and slow payment policy.

5. In the fourth quarter of 2021, taxpayers who have slowed corporate income tax have been slowed in, according to the "Announcement" regulations, the slow payment period can continue to be extended for 4 months.

According to the announcement of the 2022 Announcement, a small and medium -sized enterprise for manufacturing in the fourth quarter of 2021, the manufacturing industry, which has been slowed in corporate income tax policies, its 2021 corporate income tax settlement payable tax should be repaid with the fourth quarter of 2021. The tax paid paid was delayed and the paid was delayed. The tax could continue to be delayed for 4 months in accordance with the provisions of this "Announcement".

Example 4: Taxpay D, the quarterly prepaid corporate income tax, the corporate income tax of 100,000 yuan in the fourth quarter of 2021, according to the announcement of the 2022 announcement, the tax can be delayed to the payment of the library in October 2022 to the library to the library to the library in October 2022 Essence After the announcement of this "Announcement", its slowdown period continues to extend for 4 months, and can be paid in the warehouse in February 2023.

In addition, if the taxpayer's 2021 corporate income tax settlement is settled, the tax payable will be paid 200,000 yuan, and it can be paid in the warehouse in October 2022 according to the previous retractable policy. After the announcement of this "Announcement", it can continue to delay the entry into the library with the fourth quarter of 2021 in the fourth quarter of 2021 to February 2023.

6. Does the taxpayer enjoy the tax slowdown policy that affects the personal income tax calculation of the personal income tax for its business?

If the taxpayer who enjoys the tax slowing policy shall handle the personal income tax settlement of the personal income tax, and continue to implement the processing rules stipulated in the preliminary tax slowdown policy, that is, the taxable tax paid by the taxpayer shall be deemed to be "pre -paid tax", which will participate in the operation normally. Calculation of personal income tax settlement calculations. At the same time, the taxpayer shall pay the corresponding slow taxes and fees in accordance with the law after the expiry of the expiration period stipulated in the "Announcement".

Example 5: Taxpayer E is an individual industrial and commercial households with an annual sales of 1 million yuan. It implements the personal income tax of the accounting and declare the personal income tax on a quarterly application. The personal income tax that should be paid in the second quarter was delayed until the application period of January 2023. After the announcement of this "Announcement", the above -mentioned tax payment period continued to be extended by 4 months to May 2023. When the taxpayer applied for the personal income tax settlement of the personal income tax in 2022 before March 31, 2023, the taxable tax paid was deemed to be "pre -paid taxes", and the personal income tax refund of the personal income tax was settled normally. The calculation of taxation shall be applied for taxation before March 31, 2023. If the tax refund is required, the tax refund may be applied normally and will not be affected by the tax policy of the second quarter of 2022. At the same time, the taxpayer's previously paid taxes shall be paid during the application period in May 2023.

7. Can the manufacturing small and medium -sized enterprises enjoy the tax payment policy stipulated in this "Announcement", can it be applied for extension of taxes in accordance with the law?

Small and medium -sized enterprises that meet the conditions stipulated in this "Announcement", and if they meet the "People's Republic of China Taxation Management Law" and the implementation rules, they can apply for extension of tax payment conditions, and may apply for extension of taxes in accordance with the law.

- END -

The hustle and bustle and silence, Sichuan Tianfu Bank volunteer and Chengdu are traveling with Chengdu

At the end of August, the new round of new crown pneumonia's epidemic in Chengdu w...

Production and operation gradually restore the decline in the profit decline in the industrial enterprise in May

The latest industrial enterprises' profit data is fresh.On June 27, the website of...