After the layoffs were 10%and the valuation shrinks sharply, we talked to KLARNA for | 36 氪 Interview

Author:36 氪 Time:2022.07.07

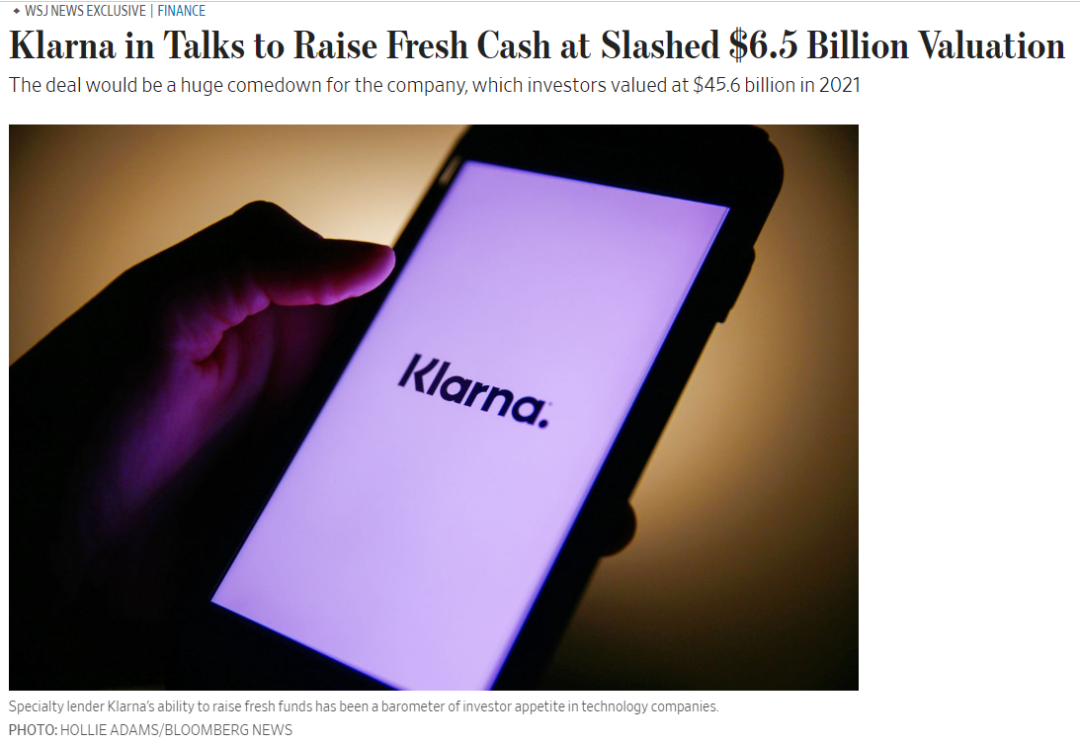

In just half a year, the valuation dived from $ 45.6 billion to less than 10 billion US dollars.

Wen | Pan Xiaoyu

Edit | Peng Xiaoqiu

Source | 36 氪 South China (ID: south_36kr)

Cover Source | IC Photo

One year ago, KLARNA received financing of SoftBank, Sequoia Capital and Yinhu Capital with a valuation of $ 45.6 billion. It shocked the global venture capital market. After all, it jumped directly into the fourth largest unicorn in the world, only after the byte beating, Stripe and Musk's SpaceX.

Earlier this year, it was still seeking new financing at a high -profile value of 50 billion US dollars. However, in just half a year, the situation turned sharply. KLARNA lowered the valuation three times. According to the Wall Street Journal, it fell from $ 30 billion to $ 15 billion and has shrunk again recently.

"Wall Street Journal" original text

In the field of payment, the listed AFFIRM and PayPal are equally difficult to be spared. AFFIRM's stock price of Nasdaq has fallen by 83%, and Paypal's stock price has fallen by 62%.

So what happened behind? There is no doubt that KLARNA has a lot of labels, but there is no shortage of questioning.

"Fintech is the biggest track of overseas valuation bubbles." Many investors told 36 氪, and KLARNA is undoubtedly a typical case, so that people evaluate their "valuation on the rocket". 10 times. But at the same time, the growth and exploration of KLARNA seems to caters to the predicament and break of global e -commerce today.

In 2005, Klarna was established in Stockholm, Sweden. At the same time, the BNPL payment model was launched overseas, that is, Buy Now Pay Later bought first and then pay. This concept was quickly detonated after the epidemic in 2020. According to a report on WorldPay, BNPL accounted for 2.1%of global e -commerce payment in 2020. For old payment companies such as PayPal, it also began to enter BNPL quickly.

Being able to quickly detonate the market is essentially the consumer of the original credit card collection. BNPL has almost no interest from consumers, but instead takes the commission to B -end users. But at the same time, BNPL will not affect the B -end merchants, because during the transaction, BNPL will pay the full amount to the merchant, and the risk of the later repayment shall be borne by it.

Obviously, the primary risk of providing BNPL is the pressure of funds. In June 2017, Klarna received a complete bank license approved by the Swedish Financial Supervision Bureau and became a personal bank. This has also become an optimal solution to the uncertainty of funds.

More than here, in the same year, KLARNA also launched its own shopping app, which also made the outside world speculate whether KLARNA wanted to be Alibaba in the European and American markets to be a platform that brings together brands. From 2B to 2C, the transformation of KLARNA is summarized as the core logic of "helping sellers to grow", and on the other hand, it is obviously inseparable from the inner volume of BNPL. As a large number of players enter the game, the proportion of commissions in the market began to be reduced, and KLARNA also needs a second growth point.

Since then, KLARNA continued to surround the C -terminal, moved to Social Shopping, and started content marketing. For a company that pays background, the distance to marketing is obviously not small. The way Klarna chooses to turn around is to acquire:

In March 2021, the acquisition of TopLooks -a company that can help merchants can help merchants on official website, social media, and KLARNA APP to create marketing content; in July, APPRL -help brands do large -scale KOL and Influenceer marketing; 7 The month also acquired Hero, a video shopping platform.

Back to the first, this set of bold attempts to be evaluated as the "Alipay+Tmall+Little Red Book" system undoubtedly won a higher return for Klarna. Since 2019, KLARNA's valuation has risen all the way, from $ 5.5 billion in 2019, to 2020 to 10 billion US dollars, ranking ten times unicorn, and then rushed to 460 in 2021 without any resistance to 460 in 2021 Estiments of 100 million dollars.

KLARNA changes the theme color is pink

But it is such a company full of ambitious and halo. On a rapidly developing highway, like global e -commerce this year, he stepped on the brakes. After pioneering a large number of markets and product innovation, Klarna was besieged in the high walls of layoffs and diving.

Just last month, KLARNA announced that it would lay off 10%. This rapidly expanding unicorn has undoubtedly reached the stage of stopping rethinking. However, the seemingly cold e -commerce market is in the stage of crossing the cycle and squeezing the foam. Whether it can bottom out and rebound is the key to measuring a company's really strong or not.

Because of this, today we talked to the person in charge of KLARNA China, Tom Xiong, and whether the passing cycle is still inseparable from the company's background. In the course of the development of KLARNA, we also tried to find the possible direction of the current e -commerce market and provide a model for global e -commerce.

The following is a dialogue between 36 氪 and Tom (edited by the editor): layoffs and emotions

36 氪: After 2020, KLARNA has developed high -speed expansion, and now it has started to lay off 10%and the valuation is diving. What do you think of this internally?

Tom: Since 2020, with market development, new products, and replenishment of new features, KLARNA has indeed opened a fast expansion mode. Although the economic environment is currently more turbulent than 2021, our overall business is still growing, especially in the Chinese market.

However, whether it is the expansion strategy during the rapid development period or the current structural adjustment, it is based on our judgment on the world situation, global economy and future expectations. So I still have hope and confidence in the future.

36 氪: When the global e -commerce is out of the period of high -speed growth, what impact your payment business has?

Tom: Although the growth rate has slowed down, I think the overseas payment market still has a great chance. After all, the change of payment methods can bring huge changes to people's lives. There is no Alipay and WeChat payment overseas. The traditional payment behavior seems very old today. For example, every time you buy stocks, deposit money or pay, consumers need to pay a lot of service fees. These funds eventually flow to banks.

So we use new technology to let users buy the same thing at a cheaper price. In fact, Klarna wants to replace the market of traditional credit cards.

36 氪: Is it a mode of replacement credit card and give you a higher valuation space?

Tom: Yes. You see the market value of overseas credit card VISA reaches more than $ 400 billion, you can compare we still have a lot of room for growth. Bank payments account for much higher GDP than domestic, but they have to collect 40%interest on users, and KLARNA is 0, which is undoubtedly more attractive to young people.

36 氪: What do you think of the Chinese market? After all, cross -border e -commerce has experienced ups and downs last year, and it is still in the cold stage.

Tom: The accident is Q1 this year, and the GMV of our Chinese market has increased by 19%. One reason is that we only opened the Chinese office last January. On the other hand, it is also the opportunity to realize BNPL in China. After using BNPL, they found that there is a higher conversion rate and customer unit price compared to the credit card payment.

Although cross -border e -commerce growth has slowed down this year, the price of traffic is more expensive than previous years. However, China's supply chain is indeed very advantageous, so it still has huge profit opportunities to make the supply chain and products well.

36 氪: How does KLARNA lay out in the Chinese market? Will it be considered to cut into the payment market by acquisition?

Tom: In an interview in China, our founder said: ‘We will never pay in China, because Chinese payment companies are too powerful, and we must not do what we want to do in China. ‘

Therefore, we still serve the DTC brand in the Chinese cross -border e -commerce industry. The 40 markets developed based on KLARNA help Chinese sellers to more markets. Of course, we will not set a clear acquisition goal, but in the way of cooperation, because China's SaaS and CRM products are not inferior to overseas products.

BNPL's imagination space

36 氪: After the concept of BNPL in 2020, a large number of payment companies began to cut into BNPL. What is the competitive point today?

Tom: In fact, the logic of BNPL between each family is the same, but the overseas and domestic situation is different. Only choose Alipay or WeChat on domestic online payment, but there are more than a dozen options when shopping overseas. Therefore, the most critical is the concept of paying the brand. Consumers will only remember one payment brand, not a bank.

36 氪: What decisions are you a payment brand?

Tom: definitely trust. This is also a matter of KLARNA. There are many independent standing overseas. People can find new brands and new independent stations on INS and Tik Tok every day. Whether or not daring to pay in the end depends on trust. And when users can return and refund on KLARNA, they can gain trust and security.

36 氪: But if the old -fashioned payment company comes to BNPL, will it be more trustworthy?

Tom: Overseas, users value you more because of what. He can trust a brand because of one thing, but this trust may not be migrated on another. This is also a consumer culture for overseas users.

36 氪: But in fact BNPL is not a strong barrier, so will the market roll up the price war quickly?

TOM: First of all, there is still a lot of opportunities in the market space. There will be no price war in the short term, but it may be in the next 7 or 8 years. At that time, it depends on who ran faster and occupied enough market share. Now, KLARNA is still the fastest.

Of course, KLARNA also expanded other businesses around BNPL itself, including installments and other products. For example, consumers will choose BNPL when buying clothing, but when buying color TVs and other appliances, they can pay 12 months in installments. For sellers, new and conversion rates are their most concerned issues, so Klarna also makes its own brand, attracting enough users on the APP to help the seller's new and transform.

Klarna's brand design

36 氪: Payment and marketing seems to be two sets of logic. Tom: data reserved on the app. For example, the VISA card knows how much their users spent every month, but it does not know which brands or products they spend more money, and they cannot tell users which products can save a sum of money. KLARNA itself is e -commerce payment, and naturally has data advantages, and more services can be carried out.

When the user opens the KLARNA App, he can see their consumption records. We can also recommend peripherals or supporting products based on the products they buy. This is the new service we can provide to merchants.

The core is to run faster

36 氪: From simple payment service to making an app for C -end, why does it change from B to C?

Tom: Our core logic is to help sellers grow. For example, a German seller sells well in Germany, but he will encounter constraints when he wants to go to the US market. And KLARNA already has enough users and brands in the United States to help him. Klarna has accumulated hundreds of millions of users in payment services.

Of course, we are optimistic about greater opportunities -overseas young people do not like credit cards, and they prefer a new way of shopping. So Klarna also positioned a more Modern payment company. What should I do? It is to do 2B and 2C to help users save money, save time, and find new brands.

36 氪: From 2B to 2C, there are actually two sets of play. Where is the difficulty here?

TOM: The difficulty is that every time we open up a new market, we need to invest a lot in the early stage. Cultivate users' habits to pay for KLARNA payment and cultivate trust.

But every local culture and language are different, and channels are different, especially in the European market. Our strength is the precise positioning and push of user portraits. We will also cooperate with our sellers to attract traffic through various discount activities.

36 氪: Do Klarna want to be an overseas version of Tmall in doing an app? What is the advantage of paying a platform for the platform?

Tom: I think it is more like a WeChat mini program compared to Tmall, because the seller can retain the data by itself, and WeChat just helps you receive the bill. Therefore, Klarna's idea is to bring together the self -standing station, but the merchant can master the CRM of the user by themselves.

The advantages of payment companies are actually data. The traffic channel can analyze the content of the user, but it is difficult to judge what it ultimately contributed to transformation. This also stems from the protection of user data overseas. So the marketing company knows what users like, but the payment company knows why users spend money.

36 氪: In addition to the app, Klarna is also doing social e -commerce.

TOM: From the perspective of the development of domestic Xiaohongshu and Douyin, there is no doubt that there is still greater opportunities in Social Shopping overseas. When helping merchants new, we also need to improve transformation through content drainage. So KLARNA also acquired Toplooks, Hero, APPRL, etc.

As for the conversion rate, there are live broadcasts with good conversion effects overseas and bad live broadcasts. In essence, because the market is highly scattered and consumer portraits are different. Therefore, what we need to master now is more localized, that is, we not only need to do content, but also need to make content that conforms to local cultural habits.

36 氪: How to achieve localization?

Tom: We have a market and content team in different countries. Usually, we will allocate a market team to the seller to determine the pioneering market, direction, and activities, and then find people who understand products and markets to discuss the final direction.

36 氪: It sounds more like a consultant model, a manpower way.

Tom: In addition to manpower, we also achieved by acquiring Internet celebrity companies and SaaS tools. But in fact, our acquisition logic is very simple, which is based on the pain points of the seller. We communicate with a large number of sellers every day.

36 氪: I understand that doing Social Shopping also means that you need a lot of traffic. How do you get traffic?

Tom: Klarna's biggest gameplay is to do brand Campaign (brand solution). We will cooperate with overseas stars, such as Lady Gaga, Snoop Dogg, and ASAP ROCKY to carry out a series of events.

36 氪: A question that can't be bypassed -Payment+APP+Marketing, the service of so many attributes, can KLARNA complete it?

Tom: So we have to run fast and occupy the market first. There are many details that need to be improved, but it is clear why we do it.

36 The official public account of its subsidiary

I sincerely recommend you to follow

Data-nickName = "36 氪 South China" data-alias = "south_36kr" data-signature = "36 氪 under the official account. Focus on the Greater Bay Area, radiate South China, connect the world with business, and let some people come first first.In the future! "Data-from =" 0 " /> to" share, watch "

- END -

WeChat emoticons are written into the judgment, is Emoji fell out of favor?

A few days ago,#WeChat emoticons were written into the judgment#This entry quietly...

Tao brand is easy, shake the brand difficult

Edit Introduction: Three Squirrels, Handu Clothing House, Yu Nifang ... Taobao has...