2022 National Double Innovation Week, take you to understand the preferential tax and fees policies of "mass entrepreneurship and innovation"

Author:State Administration of Taxati Time:2022.09.17

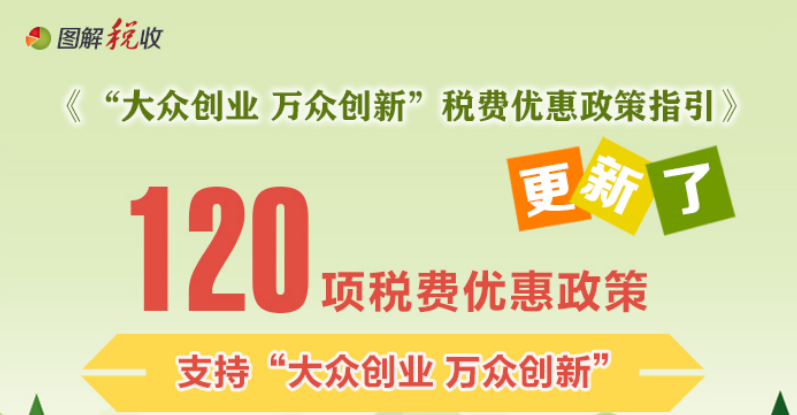

On September 15th, 2022 National Volkswagen Entrepreneurship Innovation Activities Week, with the theme of "Innovation and Entrepreneurship, Promoting Employment". In 2022, the state issued a new combined tax support policy. The State Administration of Taxation further sorted out and merged into 120 taxes and fees policies and measures around the main links and key areas of innovation and entrepreneurship, covering the entire life cycle of the enterprise. Double innovation activity week, let's learn about relevant tax and fees preferential policies together

"Volkswagen Entrepreneurship Thousands of Innovation" Tax and Feature Policy Guidelines Statement Catalog

1. Enterprise initial construction tax discount

(1) Tax and fees for small and micro enterprises

1. Small and micro enterprises reserve tax refund at the end of the value -added tax period

2. Eligible VAT small -scale taxpayers are exempt from VAT

3. VAT small -scale taxpayer phase -exempt VAT

4. Small and micro -profit enterprises to reduce corporate income tax

5. Individual industrial and commercial households pay taxes for no more than 1 million yuan in personal income tax.

6. VAT small -scale taxpayers reduce local "six taxes and two fees"

7. Small and micro -profit enterprises to reduce local "six taxes and two fees"

8. Individual industrial and commercial households reduce the "six taxes and two fees"

9. Manufacturing small and medium -sized enterprises delay paying part of taxes and fees

10. Small and medium -sized enterprises to purchase equipment appliances deducting a certain percentage of one -time tax

11.

12. Eligible enterprises to temporarily exempt the employment guarantee for the disabled

13. Eligible payment obligations exempt relevant government funds

14. Eligible enterprises to reduce employment guarantee for the disabled

15. Eligible payment obligations to reduce the construction fee of cultural business

16. Eligible VAT small -scale taxpayers are exempt from cultural business construction fees

(2) Key group entrepreneurial employment tax discounts

17. Key group entrepreneurial tax deduction deduction

18. Adding to key group employment tax deductions

19. Retired soldiers' entrepreneurial tax deduction

20. Removal of retired soldiers' employment tax deduction deduction

21. Family family members of the army are exempt from VAT for entrepreneurship

22. Personal income tax for the family members of the army

23. Enterprises that resettle the employment of the army of the army are exempt from value -added tax

24. Military -transferred cadres to start a business exempt VAT for entrepreneurship

25.

26. Enterprises that reset the army to transfer cadres to employment are exempt from VAT tax

27. Disabled people with entrepreneurship exempt VAT

28. Units and individual industrial and commercial household VATs of the disabled employment are levied immediately

29. Special education Enterprises to resettle the employment of the disabled for employment VAT will be levied immediately

30. The salary of the disabled people who resettle the employment of the disabled plus deduction

31. Units that reset the employment of disabled people to reduce urban land use tax

32. Long -term coming to China to settle in experts imported self -use car for exemption of vehicle purchase tax

33. The person who returns to the country to buy a self -use domestic car is exempted from the purchase tax of the vehicle

(3) Tax discount on entrepreneurial employment platform

34. Technology enterprise incubators and crowdsour

35. Technology enterprise incubators and crowdsiders are exempt from real estate tax

36. Technology enterprise incubators and crowd -creation space exempt urban land use tax

37. University Science and Technology Park levied VAT with VAT

38. University Science and Technology Park for Real Estate Tax

39. University Science and Technology Park is exempted from urban land use tax

(4) Investment tax discounts for entrepreneurial investment

40. Venture Capital Enterprises invest in small and medium -sized high -tech enterprises that have not been listed to deduct taxable income in proportion

41. Limited partnership Entrepreneurship investment enterprise legal person partners invest in small and medium -sized high -tech enterprises that have not been listed to deduct taxable income in proportion

42. Company -based entrepreneurial investment enterprise invests in start -up technology -based enterprises deducting taxable income

43. Limited partnership Venture Capital Corporate Legal Partners Investment of Start -up Technology -based Enterprises deduct the income from partnerships from partnerships

44. Limited partnership Venture Capital Enterprise Personal Partner Investment of start -up technology -based enterprises deduct the business income from partnerships

45. Angel Investment Personal Investment Personal Investment Enterprise deducts taxable income

46. Entrepreneurship investment enterprise flexibly selects personal partnership income tax accounting methods

47. Zhongguancun State Independent Innovation Demonstration Zone Trial Company -type Entrepreneurship Investment Enterprise Promotional Policy

48. China (Shanghai) Free Trade Pilot Zone Lingang New Trinity Zone will reduce corporate income tax in key industries

49. Pilot policy of corporate entrepreneurial investment enterprise income tax in the specific region of Pudong New District, Shanghai

(5) Financial support tax discounts

50. Innovative enterprise issued deposit vouchers pilot phase VAT preferential policies

51. Innovate the pilot stage of the issuance of deposit vouchers in the enterprise in the pilot stage of corporate income tax

52. Innovative enterprise issuance of deposit vouchers pilot stage Personal income tax preferential policies

53. Non -monetary asset transfer income of non -monetary assets undergoing non -monetary assets to pay corporate income tax in installments

54. Pay personal income tax for non -monetary asset transfer income confirmed by non -monetary assets

55. Financial institutions to small and micro enterprises and individual industrial and commercial households for small loan interest income exempt VAT

56. Financial institutions Farmers' small loan interest income income tax reduction income income

57. Financial enterprises' loan loss reserve for agriculture and small and medium -sized enterprises will be deducted before tax reserve

58. Financial enterprises' loan losses for agriculture and SMEs are deducted before taxation

59. Financial institutions signed a loan contract with small and micro -enterprises to levy stamp duty 60. Small loan company farmers' small loan interest income is exempt from VAT

61. Small loan company farmers' small loan interest income income tax reduction income income

62. Micro -loan company loan loss reserve reserves enterprise income tax for income tax deductions

63. Provide financing guarantee for farmers and small and micro -enterprises and exempt VAT for levy

64. SME financing (credit) guarantee institutions related reserve enterprise income tax will be deducted before

65. Financial institutions are exempt from value -added tax from farmers' small loan interest income

66. Agriculture and animal husbandry insurance and related technical training business projects are exempt from VAT

67. Insurance companies provide insurance income from the insurance business for the planting and breeding industry to reduce the income income income of corporate income taxes

68. Personal transfer of stocks of the Beijing Stock Exchange's listed company shares exempt VAT

69. Investment in the personal income tax policies of the Beijing Stock Exchange listed company

70. Support the infrastructure field of real estate investment trust funds (REITs) pilot preferential tax preferential tax policies

71. Support the infrastructure field of real estate investment trust funds (REITs) pilot project company corporate income tax preferential policies

72. Accounting tax duty reduction and exemption

Second, the company's growth period of tax and fee discount

(1) VAT policy of production and living service industries to reduce the policy of deducting reduction

73.

(2) R & D expenses plus deduction policy

74. R & D expenses plus deduction

75. Manufacturing enterprise R & D expenses enterprise income tax 100%plus deduction

76. Technology -based SME R & D expenses Enterprise income tax 100%plus deduction

77. Entrusted overseas R & D expenses plus deduction

(3) Fixed asset accelerated depreciation policy

78. Fixed assets accelerate depreciation or deducting one -time deduction

79. Manufacturing and some service industries comply with qualified instruments and equipment to accelerate depreciation

(4) Imported scientific research technology Equipment and supplies tax discount

80. Major technical equipment import exemption VAT -value -added tax

81. Scientific research institutions, technology development institutions, schools and other units import exemption of value -added tax, consumption tax

(5) Tax discounts for transformation of scientific and technological achievements

82. Technical transfer, technical development and related technical consulting and technical services exempt VAT

83. Technical transfer income reduction and exemption corporate income tax

84. Zhongguancun State Independent Innovation Demonstration Zone Specific Enterprise Enterprise Technology Transfer and Exemption of Enterprise Income Tax

(6) Research Innovation Talent Tax Promotion

85. Scientific research institutions and colleges and universities are extended to pay personal income tax

86. High -tech enterprise technical personnel equity awards Instalize personal income tax

87. Small and medium -sized high -tech enterprises transfer personal income tax in installments to individual shareholders

88. Get the personal income tax of non -listed companies' stock options, equity options, restricted stocks and equity awards

89. Obtained the stock options, restricted stocks and equity awards of listed companies appropriately extend the tax period

90. Enterprises and individuals invest in delayed income tax for investment in technological achievements

91. Science and technology bonuses issued by national, provincial and ministerial levels, and international organizations are exempt from personal income tax

92. Cash rewards and exemption of personal income tax in cash rewards for scientific and technological achievements

3. Promotion of taxes and fees for the maturity period of enterprise

(1) Tax discounts of high -tech enterprises and manufacturing industries

93. High -tech enterprises minus the 15 % tax rate for corporate income tax

94. High -tech enterprises and technology -based small and medium -sized enterprises have a loss of loss to 10 years

95. Technical advanced service enterprise minus a 15 % tax rate for corporate income tax

96. Eligible manufacturing industries and other industries such as taxpayers at the end of the VAT period will be repaid

(2) Software enterprise tax discounts

97. Software products VAT exceeds tax burden and return immediately

98. Software companies encouraged by the state regularly reduce corporate income tax

99. Key software companies encouraged by the state to reduce corporate income tax

100. Software companies will levy to refund value -added taxes for software product development and expand income tax policy

101. Eligible software Employee training costs are deducted from the actual amount of tax

102. Enterprise outsourcing software shortens depreciation or amortization years

(3) Integrated circuit Enterprise Tax and Features

103. Integrated circuit major project enterprises VAT tax refund

104. The value -added tax period for the refund of the integrated circuit enterprise at the end of the value -added tax period is deducted from urban maintenance construction tax, educational additional and local education additional taxation (levies) basis

105. Enterprises that undertake a major project of integrated circuits can pay import value -added tax in installments in installments

106. Integrated circuit manufacturers with a line width of less than 0.8 microns regularly reduce corporate income tax

107. Integrated circuit manufacturers with a line width of less than 0.25 microns regularly reduce corporate income tax

108. Integrated circuit manufacturers with an investment of more than 8 billion yuan regularly deduct corporate income tax

109. Integrated circuit manufacturers or projects with an investment of more than 15 billion yuan regularly reduced corporate income tax

110. Integrated circuit production enterprises or projects with a line width of the country or less than 28 nanometers are regularly reduced by enterprise income tax

111. Integrated circuit manufacturers or projects with a line width of the country or less than 65 nanometer are scored for enterprise income tax

112. Integrated circuit production enterprises or projects with a line width of the country or less than 130 nanometers are regularly reduced by enterprise income tax

113. Integrated circuit production enterprises encouraged by the country with less than 130 nanometers extend the loss of losses

114. The national encouragement of integrated circuit design, equipment, materials, packaging, and testing enterprises regularly reduce corporate income tax

115. Key integrated circuit design enterprises encouraged by the state regularly reduce corporate income tax

116. The production equipment of integrated circuit production enterprises shorten the depreciation period

(4) Tax discounts for animation enterprises

117. Sales independent development and production animation software VAT's value -added tax over tax will be levied immediately

118. Eligible anime design and other services can choose to apply a simple tax calculation method to calculate and pay VAT

119. Anime software export exemption VAT levies VAT

120. Eligible animation companies can apply for preferential policies for corporate income taxes that encourage the development of the software industry

Please check the specific content of the above -mentioned tax and fees preferential policies

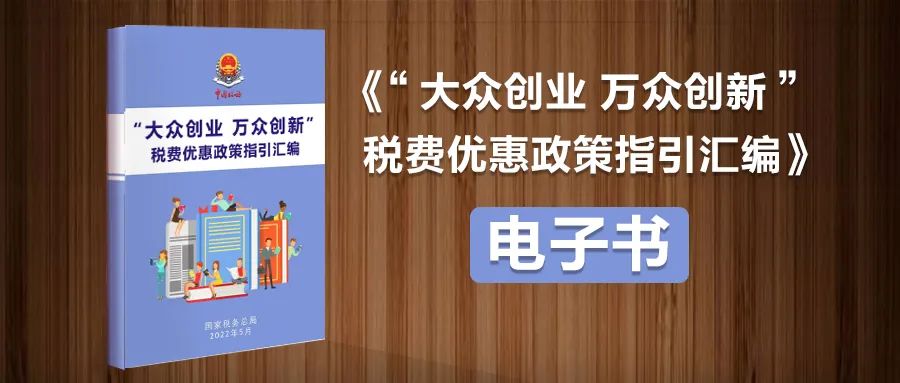

"Compilation of the Guide of" Popular Entrepreneurship "Tax and Feature Policy Guide"

You can also view e -books

Quickly turn to the little friends in need ~

- END -

Death to high temperature?Firefighters are coming to save my cub

Hey Hey heyIs it 119?My pig is about to die at high speedCan you help me help mear...

Wolong District African Swine Forestless Community successfully passed the national review and acceptance

On August 23, Fan Qinlei, a team of African Swine Fever Wuyan District of the Ministry of Agriculture and Rural Africa, and a group of 5 people, who evaluated the creation of the creation of the Afric